- EBS Investments Newsletter

- Posts

- SPGI: That Stock That Beats the Market, Market Commentary & Beginner Investing Books

SPGI: That Stock That Beats the Market, Market Commentary & Beginner Investing Books

August Edition

Bailey Erwin

September 01, 2023

SPGI Stock Analysis

By: EBS Invests

SPGI Logo (Source: https://companieslogo.com/sp-global/logo/)

Overview:

S&P Global Inc. (SPGI), along with their sister firms, provide credit ratings, analyses, benchmarks, commodity and automotive market coverage, and solutions for global capital. You may not know it, but you see them every day. They own the rights to the S&P 500 index, which tracks the top 500 companies in the US and is the basic benchmark for the entire stock market. Needless to say, SPGI is a global financial institution that has a great moat and provides services and products that many companies use.

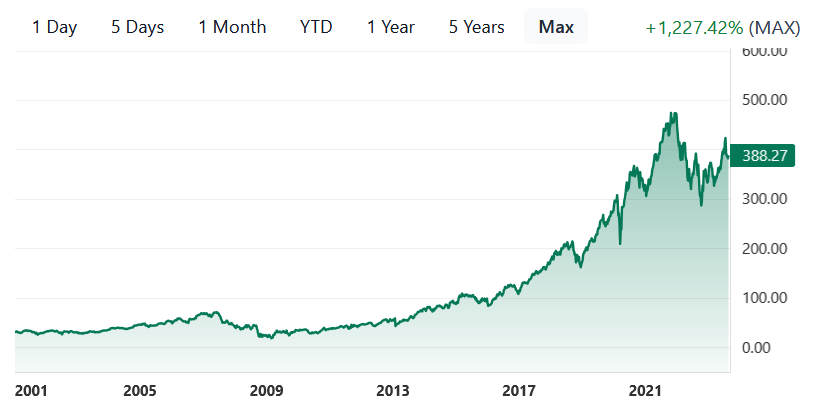

Over the past five years, SPGI has had a rate of return (RoR) of 91.96%. Whereas the S&P 500 has a RoR of 55.94%. It’s almost double what the S&P returns in the same period. They have a max gain of 1,236% since their IPO in 2001. Their business really started to take off when they acquired IHS Markit fully for $44 billion US in early 2022. IHS offers economic measures and M&A for management in different nations around the world. With the combined deal, SPGI plans to grow at roughly 6.5-8% and increase its profitability by 200 basis points. Increasing their free cash flow, and returning 85% of their free cash flow as dividends and share buybacks, while lowering their payout to roughly 20-30%. That is great news for investors.

SPGI max chart (Source: https://stockanalysis.com/stocks/spgi/)

Imagine you’re a company that wants to get listed on the New York Stock Exchange. You’ll need a credit rating and a stock ticker. Want to be listed? Well, you’ll have to pay fees to be listed on the S&P 500. SPGI is involved every step of the way. They provide companies with the keys to the stock market and get paid handsomely for it. Let’s dive into the financials and fundamentals of why I think they’re a great business.

Financials and dividend information:

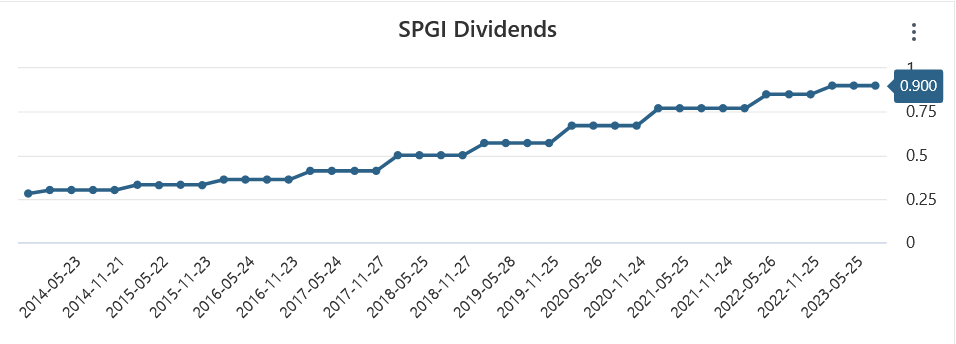

SPGI’s revenue has a 5-year compound annual growth rate (CAGR) of 14.01% and a 3-year CAGR of 16.86%. At this time, their dividend is growing at 9.57% per year. SPGI’s current payout ratio is 50%, which is near the top of where I like companies to be (the lower the payout the better). As I mentioned, they plan to decrease their payout ratio. The firm’s dividend yield (Y) is 0.92%, which is low, but when combined with their fast dividend payment increases, it’s perfectly fine.

SPGI Dividend Chart (Source: https://stockanalysis.com/stocks/spgi/dividend/)

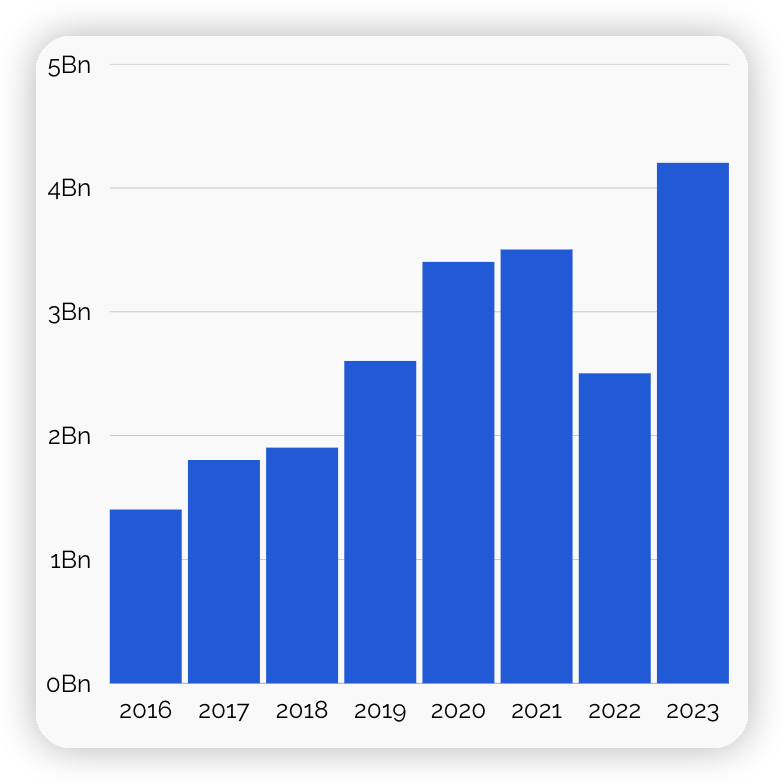

**Additionally, SPGI has some of the strongest free cash flow (FCF) growth I have seen in a company (free cash flow is the extra cash from operations, that the company can choose what to do with). SPGI for 2023 is projecting $4.2 billion US in free cash flow. Up $1.7 billion US from 2022. To be fair, 2022 had a drop-off in FCF due to the bear market. Discounting 2022, 2023 is expected to be up $.7billion from 2021. That is roughly 17% growth, showing strong growing cash flows, which I attribute to their solid management and their recent acquisition. The 2023 projections show that the company is rebounding quickly, especially given the current economic climate.

SPGI Free Cash Flow Chart (Data: https://stockanalysis.com/stocks/spgi/financials/cash-flow-statement/. Forward projections https://www.msn.com/en-us/money/companies/s-p-global-spgi-q2-2023-earnings-call-transcript/ar-AA1erSYF)

Valuation:

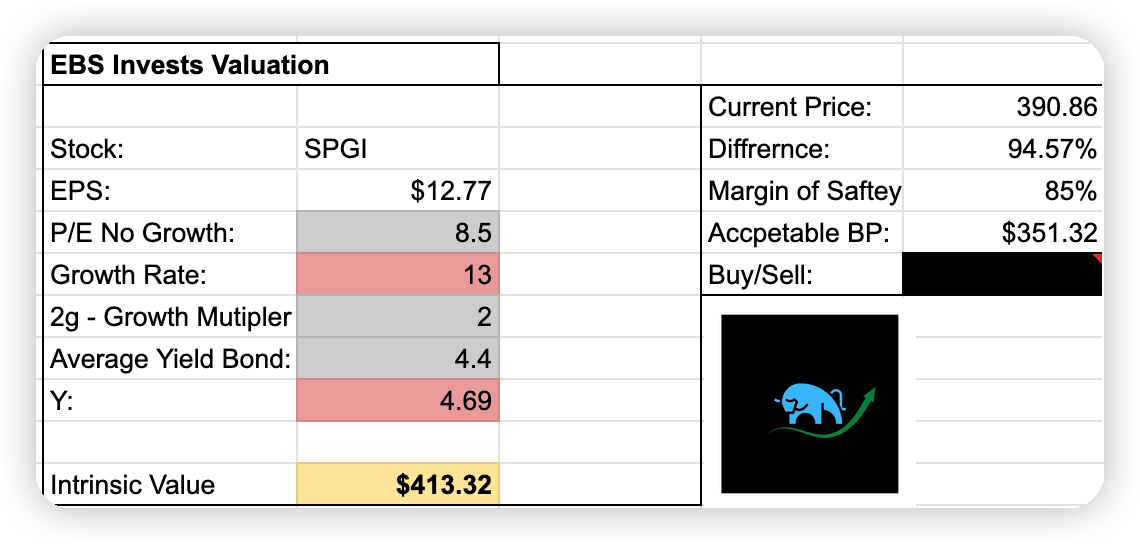

SPGI is regarded as an expensive stock. The firm has a PE of 54, much higher than most people should consider. Even in the industry, SPGI has the highest PE, with the average for the industry being 48. Although SPGI has a higher PE, the entire industry has high PEs. I do encourage you to not be blindsided by the PE. SPGI has outstanding revenue, dividends and FCF growth. Furthermore, SPGI stock has fallen ~8.7% since its high in July.

Applying a 13% growth rate, which is fair for the company and its growth, I also used the EPS projections for 2023 which is expected to be $12.77. With these numbers, I get a value of $413. This company rarely goes on sale, because when the market is bullish, SPGI follows suit as they own the S&P. With a 15% margin of safety (MOS), I get a buy price of $351. The stock has some distance to fall before then. I personally think anytime you can pick up this stock below $380, it’s not a bad deal. This stock is a real compounder, and I feel it will take it off before hitting those low of numbers.

EBS Invests IVC

Conclusion:

SPGI is a strong stock for your portfolio. It offers a really strong business that we should take advantage of. Furthermore, with their recent acquisition of IHS Markit they have more growth ahead. This acquisition also helps them by providing great diversification for them. When I look for stocks that are great in my portfolio, I look for growing revenue, growing dividend, a moat that sets it aside from the competition, and growing free cash flow. SPGI offers all of that. SPGI should find a nice spot in your portfolio as a strong compounder that you need.

Market Commentary Regarding NVDA

Nvidia (NVDA) is the new, fresh thing every investor wants. Their stock has been on a tear in 2023, up 244%. They have more than doubled their revenue in Q2 of 2023. Their chips, which power AI solutions and video game consoles, are regarded as the best in the industry. They are a well-positioned company for the future and poised for growth.

As investors, we must remain diligent. We must not get FOMO (fear of missing out). Yes, NVDA stock has been reaching new highs almost every week. However, their PE is 120, overvalued by wide margins. They also provide low to almost no dividend growth. Furthermore, the AI bubble is here. These high-flying tech stocks can only go on so long.

I will consider buying NVDA if it falls roughly 15%. For now, the price is too expensive and doesn’t justify their market cap or PE. Additionally, I own NVDA via my ETFs that track the S&P, I believe I have enough exposure through that.

Question of the Edition:

Q: I was wondering if you could recommend an investing book for me to start learning about investing?

A: I have read multiple books about the world of investing. My two favorites that teach the fundamentals that every person should read are in this order below.

Rich Dad Poor Dad, by: Robert Kiyosaki and Sharon L. Lechter

This book fixed everything with me in regard to money and how I spend my time. In my opinion, this book taught me real-life opportunity cost decisions. I used to spend thousands and save little, but now my savings are larger than many teenagers can dream. You will never be successful in life unless you get your finances under control; this book teaches that.

The Little Book of Common Sense Investing, by: John C Bogle

It is my strong opinion that most people should not invest in individual stocks. The majority of people pick poor stocks and never beat the market. The book teaches you to only invest in the S&P index funds to get your fair share of stock market returns.

Stock purchases and dividends, July 16th-Aug 31:

Purchases:

ALB - $92

AXP - $80

CP - 1 share

MSFT - $53

SCHD - 4 shares

SCHX - 1 share

TGT - $44

TROW - $20

QCOM - $20

UNH - $13

Dividends:

AAPL - $0.51

AXP - $0.88

JPM - $1.42

SBUX - $1.39

SCHW - $0.99

SWVXX - $17.66

Total in period (7/15-8/31): $22.85

YTD Total: $203.48

Want to Read Past Editions? Click Below:

Have a question or comment? Email me:

//See you in the next edition

EBS Invests 2023//

NOT A FINANCIAL ADVISOR.

**The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our site constitutes a solicitation, recommendation, endorsement, or offer by EBS Invests (Investments) or any third party provided to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such an offer would be unlawful under the securities laws or such jurisdiction.

There are risks associated with investing in securities. Investing in stocks, bonds, ETFs, mutual funds all involve a risk of loss. **